Escape The Retirement Tax Trap Most Miss

If Most Of Your Wealth Is In A 401(k), Read This Before Retirement

How pre-retirees with $250K+ in tax-deferred savings are generating income the IRS can’t touch — income that doesn’t inflate your Medicare premiums, doesn’t trigger RMDs, and doesn’t disappear when the market drops.

Live Online July 1st

At 3PM CST/ 4PM EST

Escape The Retirement Tax Trap Most Miss

If Most Of Your Wealth Is In A 401(k), Read This Before Retirement

How pre-retirees with $250K+ in tax-deferred savings are generating income the IRS can’t touch — income that doesn’t inflate your Medicare premiums, doesn’t trigger RMDs, and doesn’t disappear when the market drops. Discover how to identify hidden financial inefficiencies that may be quietly costing you thousands over time.

Live Online July 1st

At 3PM CST/ 4PM EST

The Problem Most Advisors Won’t Name

Your 401(k) Isn’t a Retirement Account.

It’s a Deferred Tax Account.

You spent decades building this nest egg. What no one told you: the IRS is your silent business partner — with a mandatory withdrawal schedule that begins at 73 whether you need the money or not. And every dollar you pull triggers a chain reaction most people never see coming until it’s too late to plan around it.

Save your seat now.

Your future self will thank you.

The Problem Most Advisors Won’t Name

Your 401(k) Isn’t a Retirement Account.

It’s a Deferred Tax Account.

Here’s what you may be facing:

The RMD Trap -At 73, the IRS mandates how much you withdraw from your IRA or 401(k) — and taxes every dollar as ordinary income. You don’t get to choose the timing. The government does

The Social Security Surprise -Up to 85% of your Social Security benefit is taxable. Most pre-retirees discover this on their first post-retirement tax return — after it’s already too late to plan around it.

The Medicare Surcharge -IRMAA kicks in at $103K for individuals. One Roth conversion, one RMD, and one Social Security payment in the same year can push you over the line and add $1,500–$5,000+ annually to your Medicare premiums.

The Bracket Illusion -I’ll be in a lower bracket in retirement.” When RMDs, Social Security, and Medicare stack simultaneously, many retirees land in the same bracket — or higher — than their working years.

Late-night research increases awareness but creates more confusion

Hesitation to act due to fear of making the wrong decision

Don’t miss this free info session — it could save you thousands.

Date: July 1st

Time: 3pm CST / 4pm EST

Duration: 60 minutes

Tuesday, July 1st 3pm CST / 4pm EST

To change and reuse text themes, go to Site Styles.

What You’ll Walk Away With

60 Minutes That Could Change What

Your Retirement Actually Costs You

This isn’t a sales presentation. It’s the strategy review your financial advisor should have given you — and didn’t.

The IRS-recognized vehicle most advisors never discuss — and why it produces retirement income that doesn’t appear on your AGI, doesn’t trigger Medicare surcharges, and isn’t subject to RMDs.

Why a Roth IRA alone isn’t a tax strategy — it’s a tactic without architecture. You’ll see what a complete distribution-phase income plan actually looks like when it’s built correctly.

A real side-by-side illustration of what a traditional 401(k) withdrawal plan costs in taxes over 20 years versus a repositioning strategy built before retirement begins.

The IRC code sections that make tax-free retirement income legal, documented, and IRS-approved — not a loophole, not a workaround. Architecture that has been in the code since 1984.

How to know if you still have the window — this strategy works best for those 5–15 years from retirement. Matt will show you exactly how to read your own timeline and what your options still are.

What the wealthiest retirees actually retire out of — and why it’s almost never the account they were told to maximize during their working years.

Save your seat now.

Your future self will thank you.

What Most People Believe vs. What the Numbers Say

The Wrong Beliefs That Are

Costing You Right Now

Common Belief

“I’ll be in a lower tax bracket when I retire.”

RMDs, Social Security income, and Medicare surcharges stack simultaneously. Most pre-retirees are shocked by the real combined number.

✓ What the Math Shows

Many retirees land in the same bracket — or higher — than their working years.

Without a coordinated income strategy, the distribution phase often costs more than anyone projected going in.

Common Belief

“My financial advisor has a tax plan for me.”

Advisors manage investments. Tax strategy is a separate discipline — and most aren’t trained or licensed to execute it.

✓ What the Math Shows

Investment management and retirement tax planning are two different jobs.

If you can’t name the person who manages your retirement tax exposure, that job is almost certainly not being done.

Common Belief

“Life insurance is for death — not retirement income.”

This is the most expensive misconception in retirement planning. Most people have never seen this vehicle modeled correctly.

✓ What the Math Shows

Under IRC Section 7702, properly structured CVLI produces income that is tax-free, IRMAA-invisible, and RMD-exempt.

It has been in the tax code since 1984. The wealthiest retirees in America have used it for decades.

Tuesday, July 1st 3pm CST / 4pm EST

To change and reuse text themes, go to Site Styles.

Is this webinar for you?

This Was Built for You If…

You have $250K+ in a 401(k), IRA, or retirement account

The larger the tax-deferred balance, the larger the future exposure. If most of your savings is pre-tax, this session is built for your situation.

You’re 50–65, within 5–15 years of retirement or recently retired

Close enough to feel the urgency. Far enough that there’s still a meaningful window to act. This is the implementation zone.

You’ve wondered what you’ll actually keep after taxes

Your advisor showed you a pre-tax projection. This webinar shows you the after-tax reality — and what you can still do about it.

You want education, not another sales pitch

If you’ve sat through dinner seminars that promised answers and delivered products, this is different. We show you the math. You decide.

David Quaglia

Retirement Income Specialist · Tax-Free Income Strategist

David Quaglia has spent his career doing one thing: helping pre-retirees and retirees understand what their money is actually worth after taxes — and building strategies that close the gap between the number their advisor showed them and the income they actually keep.

He specializes in tax-advantaged income strategies for people with $250K–$2M in tax-deferred assets who are close enough to retirement to feel the urgency, and far enough away to still do something meaningful about it. His approach is math-first, jargon-free, and built on one principle: you can’t plan around what you don’t understand.

► Retirement income specialist with a focused practice in tax-free distribution planning

► Expert in indexed universal life as a retirement income vehicle under IRC Section 7702

► Has helped clients across the country model and implement coordinated retirement income strategies

► Known for translating complex tax law into plain-language decisions people can actually act on

► Trusted by pre-retirees who’ve outgrown generic advice and want a strategy built for their actual numbers.

Our Promise to You

No Pitch. No Pressure. No Wasted Hour.

🛡

The Straight-Talk Guarantee

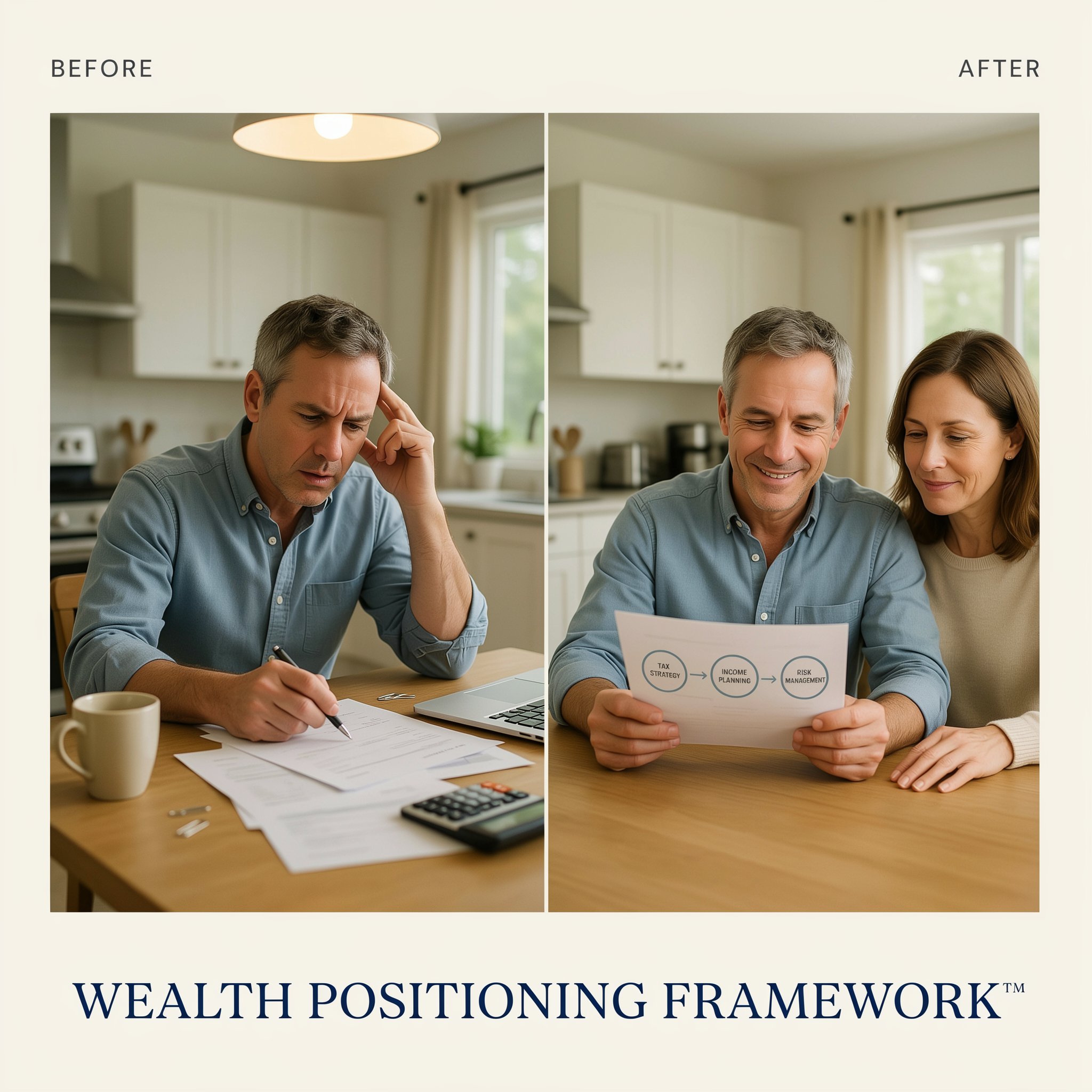

This webinar will not be a 60-minute product pitch with a soft education wrapper around it. David will show you real numbers, the Wealth Positioning Framework™, and a real before-and-after illustration of what a coordinated retirement tax strategy looks like versus the default plan.

If you attend and don’t walk away with at least one insight your current advisor hasn’t given you, we’ve failed. That’s the standard we hold ourselves to — and why we’re not afraid to invite your skepticism in the door.

“The wealthy don’t retire out of their 401(k).

They retire out of vehicles their accountant helped them build decades earlier.”

This webinar shows you what that vehicle looks like — and whether you still have the window to build it.

©2026 The Compass Wealth Group, LLC All Rights Reserved

Privacy Policy | Terms & Conditins

Contact us at: {CONTACT INFO}

©2026 The Compass Wealth Group, LLC

All Rights Reserved

Privacy Policy | Terms & Conditins

This site is not a part of the Facebook website or Facebook, Inc. Additionally, this site is not endorsed by Facebook in any way. FACEBOOK is a trademark of FACEBOOK, Inc.

By submitting your email address and phone number on this website, you are authorizing our company to send you informational and promotional messages via email, phone calls, and text messages.